Benefits of a Jumbo Loan for High-end Realty Purchases

Benefits of a Jumbo Loan for High-end Realty Purchases

Blog Article

Recognizing What a Jumbo Financing Entails and How It Differs From Conventional Car Loans

Navigating the complexities of jumbo fundings exposes a funding choice tailored for those venturing into high-value real estate, generally exceeding the restrictions set by the Federal Housing Finance Agency. On the other hand, conventional lendings are often much more available, benefiting from support by entities such as Fannie Mae and Freddie Mac. The significant danger associated with jumbo loans requires a lot more strict qualification requirements, consisting of higher credit history and significant down payments. As these 2 loan kinds cater to varying economic landscapes, comprehending their nuances is critical for making notified choices in the complicated globe of property financing. Yet exactly how do you determine which course best matches your financial strategy?

Meaning of Jumbo Finances

Jumbo lendings are a sort of home loan that exceed the adapting lending limits established by the Federal Housing Money Agency (FHFA) These finances satisfy customers who require to finance residential or commercial properties that are more expensive than what standard loan restrictions permit. The FHFA develops annual adhering funding restrictions, and any kind of loan surpassing these thresholds is classified as a jumbo car loan.

Normally, big finances are used in high-cost genuine estate markets where home rates considerably surpass nationwide standards, such as in cities or deluxe housing sectors. As these loans are not qualified for purchase by Fannie Mae or Freddie Mac, they carry fundamental threats for lending institutions as a result of their bigger size and non-conformity (jumbo loan). Lending institutions commonly impose extra rigid qualification standards for jumbo loans than common conforming loans.

Debtors seeking big car loans have to normally show a strong economic account, including a greater debt score, durable income verification, and significant deposit, usually 20% or more. In addition, lenders might call for much more considerable paperwork to examine the borrower's capability to take care of larger regular monthly settlements. Understanding the certain features of jumbo fundings is crucial for potential debtors browsing this segment of the home loan market.

Traditional Lendings Summary

While big financings accommodate high-value residential property funding, conventional finances represent the more common mortgage choice in the housing market. These fundings are not guaranteed or ensured by any government entity, such as the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA) Instead, they are backed by private lenders and stick to standards set by government-sponsored ventures (GSEs) like Fannie Mae and Freddie Mac.

Conventional loans are commonly supplied with dealt with or flexible rate of interest and vary in terms of period, generally extending 15 to thirty years. Debtors typically like traditional car loans for their predictable monthly payments, which can facilitate lasting monetary planning. Additionally, they are readily available for main residences, 2nd homes, and financial investment residential or commercial properties, offering adaptability to satisfy diverse consumer demands.

Trick Distinctions In Between Fundings

Understanding the nuances in between various kinds of lendings is vital for possible homebuyers navigating the complicated home loan landscape. At the center of this decision-making process are conventional car loans and jumbo fundings, each having distinctive features and offering various borrower needs. The primary distinction relaxes in the car loan amount. Jumbo car loans surpass the adhering finance limits established by the Federal Real Estate Money Firm (FHFA), which differ by region. In contrast, traditional fundings follow these limitations and are normally bought by government-sponsored entities like Fannie Mae and Freddie Mac.

Additionally, my sources the down repayment needs can vary substantially. Jumbo fundings generally call for bigger deposits, sometimes surpassing 20%, to alleviate danger. Standard financings, conversely, might permit reduced down settlements, with some programs approving just 3% for professional customers.

Credentials Needs

Safeguarding a big lending includes satisfying much more strict qualification requirements compared to standard financings, mirroring the see this page raised threat to loan providers. These finances, which go beyond the adjusting financing restrictions established by the Federal Housing Finance Firm (FHFA), are not qualified for acquisition by Freddie Mac or Fannie Mae, therefore subjecting loan providers to greater economic danger - jumbo loan. Consequently, consumers need to show a high credit reliability and financial security

A robust credit history, usually 700 or higher, is critical for authorization. Lenders also anticipate a lower debt-to-income (DTI) proportion, commonly not going beyond 43%, making sure that customers can take care of considerable monthly settlements together with various other monetary commitments. A significant money get is normally required, frequently amounting to 6 months of mortgage repayments, to reassure loan providers of the consumer's financial durability.

Down settlement expectations are likewise raised, regularly starting at 20% or even more of the home's worth. While this is a guard for lenders, it requires substantial ahead of time capital from debtors. In addition, evidence of consistent, sufficient earnings is essential, typically confirmed with tax obligation returns, W-2s, and current pay stubs. Independent individuals may need to supply more documents, such as earnings and loss declarations, to confirm their income stability.

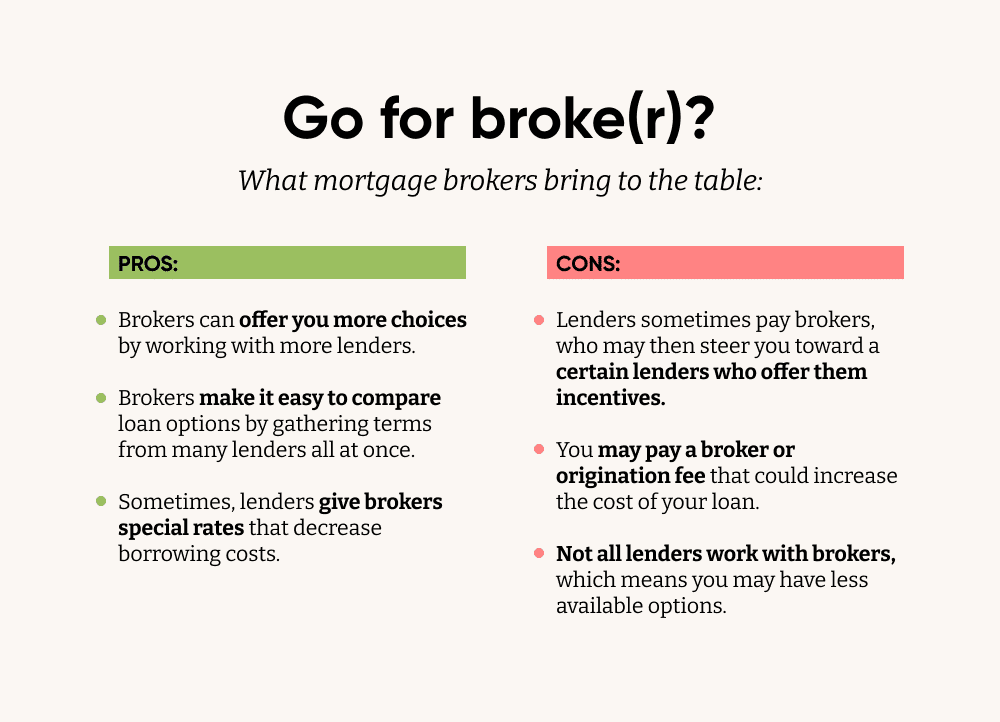

Choosing the Right Lending

Navigating the complexity of jumbo car loans needs careful consideration when picking one of the most appropriate finance choice. With the broader variety of choices offered to those seeking big finances, the decision-making procedure ought to involve a thorough evaluation of one's financial account and long-lasting goals. Unlike conventional lendings, big finances typically come with more stringent demands and differed rates of interest, which demand complete research and a clear understanding of one's economic standing.

When selecting between different big loan offerings, get redirected here it is imperative to evaluate the loan terms, consisting of interest prices, settlement schedules, and linked fees. Consumers need to contrast the prices supplied by various loan providers to guarantee they protect the most positive terms. Additionally, comprehending the effects of dealt with versus variable-rate mortgages (ARMs) is vital, as each alternative presents unique advantages and risks relying on market problems and individual economic approaches.

Engaging with a financial advisor or home loan broker can give beneficial understandings customized to individual conditions. These experts can aid in navigating the subtleties of big fundings, making certain that debtors are educated and geared up to choose a car loan that lines up with their monetary purposes, eventually assisting in a smoother home-buying procedure.

Final Thought

In summary, jumbo fundings act as a financial tool for obtaining high-value homes, demanding rigorous eligibility requirements and greater rates of interest as a result of the raised risk for lenders. Unlike standard fundings, which adapt FHFA limits and might obtain backing from Fannie Mae or Freddie Mac, jumbo car loans require a minimal credit history of 700 and significant down settlements. Comprehending these differences is important for debtors in high-cost actual estate markets to figure out one of the most ideal financing option for their needs.

The FHFA establishes yearly conforming finance restrictions, and any type of finance exceeding these thresholds is categorized as a jumbo finance.

At the center of this decision-making process are big car loans and conventional lendings, each having distinctive qualities and serving various customer requirements.Safeguarding a jumbo funding involves satisfying more rigid qualification demands compared to conventional car loans, reflecting the boosted threat to lenders. Unlike traditional lendings, jumbo car loans often come with more stringent requirements and varied passion rates, which require comprehensive research study and a clear understanding of one's economic standing.

Unlike conventional loans, which conform to FHFA restrictions and may receive support from Fannie Mae or Freddie Mac, big lendings call for a minimum debt rating of 700 and significant down repayments.

Report this page